Florida Alert: Home Hardening Sales Exemption

March 2022

February 2022

December 2021

November 2021

October 2021

Mixed Messages: Data Devil is in the Details

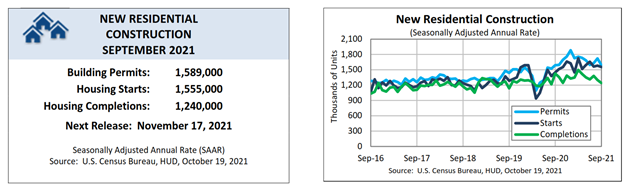

New Housing Economy

Single-family housing starts held steady in September while multi-family production dropped, resulting in an overall drop in housing unit starts of 1.6%. The Department of Housing and Urban Development, and the U.S. Census Bureau reported an annualized rate of 1.56 million units; that figure represents an annual rate should that level continue. Even with the flat production level in September, single-family starts in 2021 are 20.5% higher year-to-date

Building material pricing and other supply chain issues are cited as key factors in maintaining the construction economy.

“Single-family construction continued along recent, more sustainable trends in September,” said Chuck Fowke, chairman of the National Association of Home Builders (NAHB) and a custom home builder from Tampa, Fla. “Lumber prices have moved off recent lows, but the cost and availability of many building materials continues to be a challenge for a market that still lacks inventory. Policymakers should continue to work to improve supply-chains.”

“Builder confidence increased in October, which confirms stabilization of home construction at current levels,” said NAHB Chief Economist Robert Dietz. “The number of single-family units in the construction pipeline is 712,000, almost 31% higher than a year ago as more inventory is headed to market. Multifamily construction has expanded as well, with almost a 6% year-over-year gain for apartments currently under construction.”

A recent NAHB blog post illustrates the impact. “Despite the increase, builders are getting increasingly concerned about affordability hurdles ahead for most buyers,” the NAHB wrote on its blog. “Building material price increases and bottlenecks persist and interest rates are expected to rise in coming months as the Fed begins to taper its purchase of U.S. Treasuries and mortgage-backed debt.”

A note of caution: permit activity fell in September, possibly signaling a declining market ahead; multi-family permits dropped 18.3% in September while single-family fell 0.9%.

Labor availability also affects the construction sector. According to the U.S. Department of Labor Statistics, construction employment increased by 22,000 jobs in September but has shown little net change thus far this year. Employment in construction is still 201,000 below its February 2020 level.

For more info, visit: https://www.nahb.org/news-and-economics/industry-news/press-releases/2021/10/single-family-starts-flat-in-september

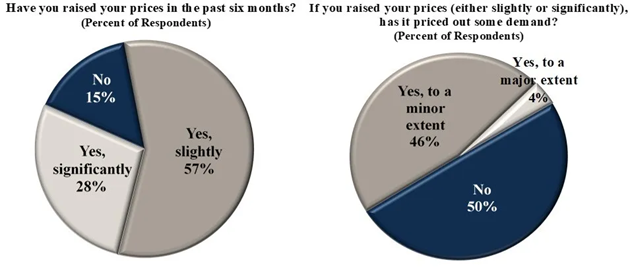

Residential Remodeling Market

The NAHB reported that the NAHB/Royal Building Products Remodeling Market Index (RMI) for the third quarter of 2021 was up five points from the third quarter of 2020, with an index of 87. The reading indicates positive residential remodeler sentiment, across all project sizes.

The RMI is based on a comprehensive survey of remodeling contractors. The third quarter survey returned some interesting takeaways concerning labor availability and material costs, and the impact on the remodeling market.

“There is strong demand and continued optimism in the residential remodeling market, despite the fact that supply constraints are severe and widespread. For example, well over 90% of remodelers in the third quarter RMI survey reported a shortage of carpenters. And 57% of remodelers reported having slightly raised prices for projects over the last six months, with another 28% indicating a significant increase in price, due in part to higher material costs and ongoing strong demand. Half of these remodelers reported some pricing out of demand due to higher prices for remodeling projects.”

Source: eyeonhousing.org

For more info visit: https://eyeonhousing.org/2021/10/remodeling-industry-confidence-improves-year-over-year-2/

Existing Home Market

The National Association of Realtors reported that September showed increased home resale values across all U.S. regions. The highlights from September include:

- Existing-home sales in the U.S. increased 7% in September from August, on a seasonally adjusted annual rate, with all regions showing an increase.

- The inventory of unsold homes decreased 13% to 1.27 million compared to 2020, and inventory dipped 0.8% compared to August.

- Median existing-home sales prices rose 13.3% above 2020 levels to $352,800.

According to NAR, the mortgage market is directly impacting existing home sales. “Some improvement in supply during prior months helped nudge up sales in September,” said Lawrence Yun, NAR’s chief economist. “Housing demand remains strong as buyers likely want to secure a home before mortgage rates increase even further next year.”

For more info visit: https://www.nar.realtor/newsroom/existing-home-sales-ascend-7-0-in-september

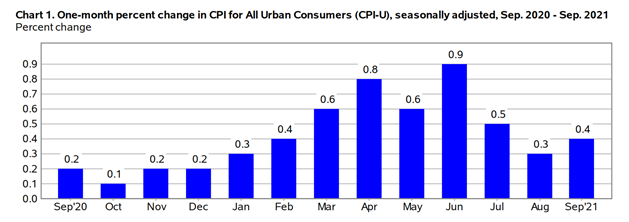

Consumer Price Index Increases

The U.S. Bureau of Labor Statistics reported that the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in September. Over the last 12 months, the “all items” index increased 5.4 percent before seasonal adjustment.

For more info visit: https://www.bls.gov/news.release/pdf/cpi.pdf

September 2021

August 2021

July 2021

IDA Industry Affairs July 2021

Midway Through 2021: Building and Construction Economy Remains Strong, But…

Supply Chain Issues Continue to Restrain Further Growth

First Half Review

The first six months of 2021 U.S. construction activity are in the books, and the news is mostly good. According to Dodge Data and Analytics, commercial and multifamily starts in the top 20 metropolitan areas of the U.S. gained 12% in value during the first six months of 2021, compared to the first half of 2020. Commercial and multifamily construction starts in the U.S. were up 10% year-to-date through six months. In the top 10 metro areas within the U.S. through June, commercial and multifamily construction starts were up 12% with only three metro areas (Washington, DC; Los Angeles, CA; and Austin, TX) showing declines.

Construction moratoriums and project delays hit many of the country’s largest cities during the beginning stages of the pandemic, resulting in very low construction activity in April and May 2020. While that 2020 drop makes the 2021 data look more favorable, the overall trend is positive.

For more info see: Construction.com

Residential Construction

New residential construction increased in June with housing starts up 6.3%. The catch? Building permits dropped in June, a sign that we will likely see a decline in housing starts in months to come. The NAHB blames supply chain issues for the weakened permit activity.

“While lumber prices have just recently begun to trend downward, builders continue to deal with rising prices of other building materials, such as oriented strand board, and major delays in the delivery of these goods,” said Chuck Fowke, chairman of the National Association of Home Builders (NAHB) and a custom home builder from Tampa, FL, “We are thankful that the White House recently held a meeting to seek solutions to these supply chain issues that are harming housing affordability.”

“The recent weakening of single-family and multifamily permits is due to higher material costs, which have pushed new home prices higher since the end of last year,” said NAHB Chief Economist Robert Dietz. “This is a challenge for a housing market that needs additional inventory.”

Non-residential Spending

Construction activity through June 2021 for non-residential projects in the U.S. shows signs of recovery. While still down 11% on a year to date basis, the volume of spending in June 2021 was up more then 14% from May.

For more info, see: Construct Connect

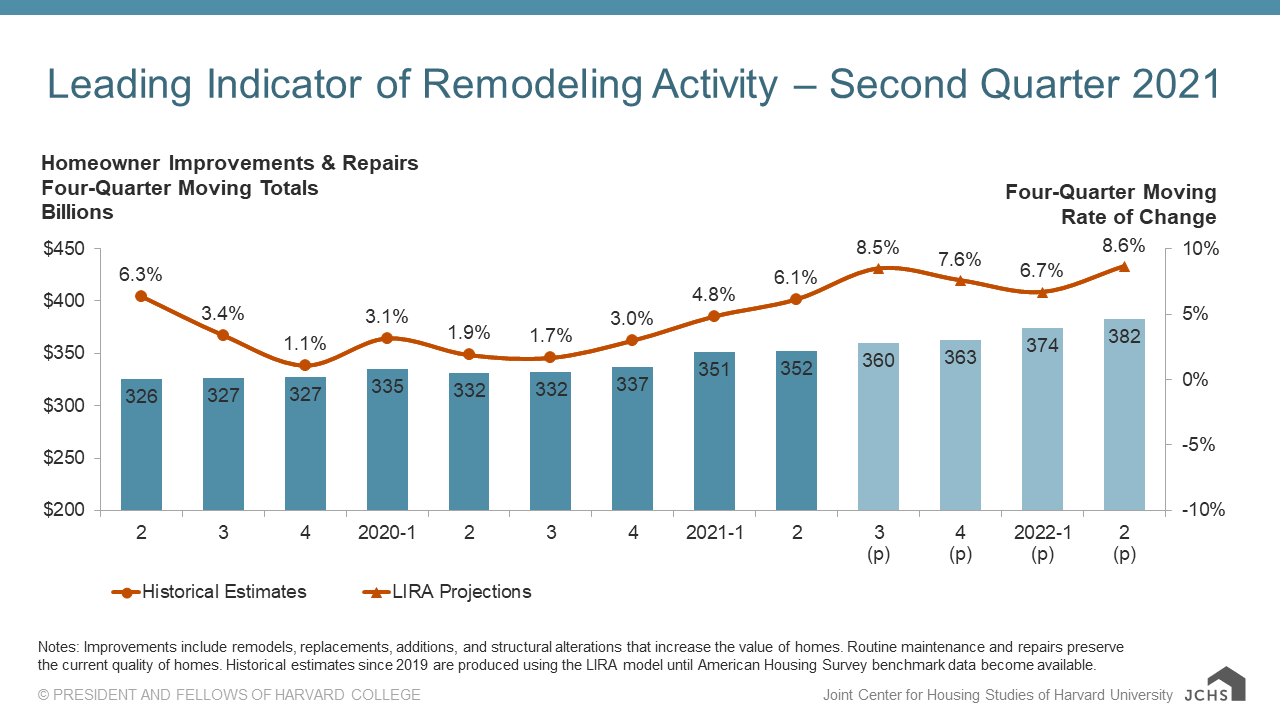

Residential Remodeling

Spending for homeowner improvement and maintenance are likely to increase through 2021 and remain strong through mid-year 2022, according to the Leading Indicator of Remodeling Activity (LIRA) from the Joint Center for Housing Studies of Harvard University. LIRA projects an 8.6% annual growth in home renovation and repair expenditures over the next year.

“Home remodeling will likely grow at a faster pace given the ongoing strength of home sales, house price appreciation, and new residential construction activity,” says Chris Herbert, Managing Director of the Joint Center for Housing Studies in a recent media release. “A significant rise in permits for home improvements also indicates that owners are continuing to invest in bigger discretionary and replacement projects.”

It’s not just about contractor remodeling, however. “Larger gains in retail sales of building materials suggest the remodeling market continues to be lifted by DIY activity as well,” says Abbe Will, Associate Project Director in the Remodeling Futures Program at the Center.

For more info see: National Association of Home Builders (NAHB), and the Joint Center for Housing Studies of Harvard University (JCHS) of Harvard University

Workforce Issues

Construction unemployment and employment in the U.S. are showing marked improvements over last year. While not back to the pre-pandemic level, it does seem to show that at least part of the two-pronged supply chain factors- materials and labor shortages- are on the way to recovery, according to the Associated Builders and Contractors (ABC).

“The widespread availability of COVID-19 vaccines and the economy’s bounce back are boosting the construction industry,” said Bernard M. Markstein, Ph.D., president, and chief economist of Markstein Advisors, who conducted the analysis for ABC. “The strength of the economic recovery will be tested in coming months by the delta variant and as the outflow of funds from the American Rescue Plan Act starts to dry up. Congress is working to address the nation’s long-standing need to repair and upgrade its infrastructure, and a qualified workforce will be necessary to get the infrastructure built. Yet a skilled workforce shortage persists. If a commonsense, bipartisan infrastructure bill is enacted into law, the economy, the construction industry and the construction workforce will benefit.”

For more info see: Contractor Magazine

https://www.contractormag.com/construction-data/article/21170860/abc-construction-unemployment-rates-down-in-45-states

The U.S. Department of Labor announced a rule rescission of Joint Employer Status rule. Here is the press release:

The U.S. Department of Labor today announced a final rule to rescind an earlier rule, “Joint Employer Status under the Fair Labor Standards Act” that took effect in March 2020. By rescinding that rule, the Department will ensure more workers receive minimum wage and overtime protections of the Fair Labor Standards Act.

The rescinded rule included a description of joint employment contrary to statutory language and Congressional intent. The rule also failed to take into account the department’s prior joint employment guidance. The U.S. District Court for the Southern District of New York vacated most of the rule in 2020.

Under the FLSA, an employee can have more than one employer for the work they perform. Joint employment applies when – for the purposes of minimum wage and overtime requirements – the department considers two separate companies to be a worker’s employer for the same work. For example, a joint employer relationship could occur where a hotel contracts with a staffing agency to provide cleaning staff, which the hotel directly controls. If the agency and the hotel are joint employers, they are both responsible for worker protections.

A strong joint employer standard is critical because FLSA responsibilities and liability for worker protections do not apply to a business that does not meet the definition of employer.

The final rule becomes effective September 28, 2021.

For more information about the FLSA or other laws it enforces, visit the Wage and Hour Division, or call toll-free 1-866-4US-WAGE.

The National Association of Manufacturers filed comments in opposition to the rule rescission. While the change will impact manufacturing, the effects will likely be felt across most industries, including construction, retail, hospitality, and service economies.

For more information visit: U.S. Department of Labor